Key takeaways

- Bank coverage determines which customers can approve and manage PayTo agreements through their banking app.

- Customers approve agreements by reviewing details and authorising through their bank.

- Agreements can be viewed, paused or cancelled by customers directly in their banking experience.

- Clear checkout and invoice messaging builds trust and reduces support questions.

- Fallback options like PayID or card ensure every customer can complete their payment.

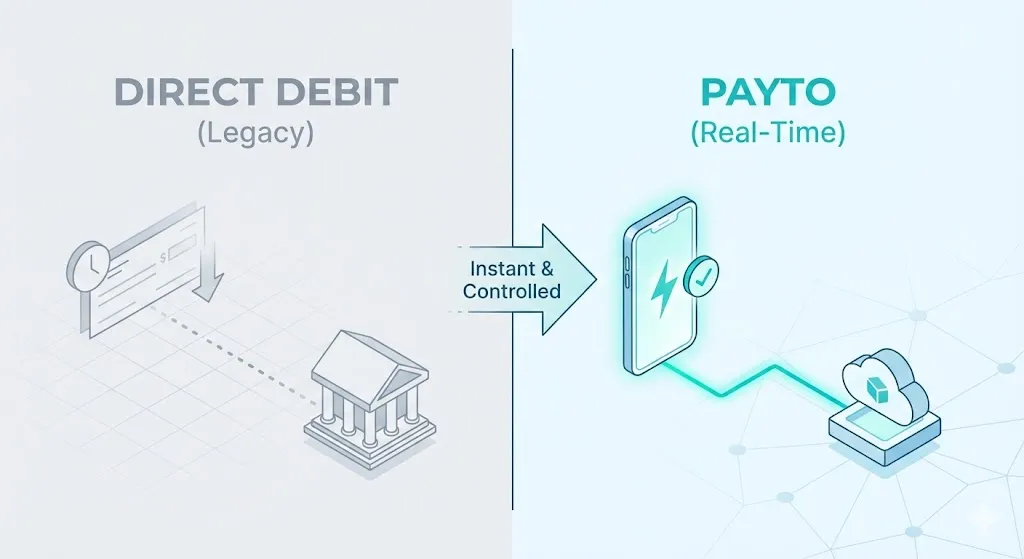

What bank coverage means

Bank coverage refers to which financial institutions have enabled PayTo for their customers. As adoption grows across Australia, more banks are supporting PayTo agreement creation and management. Coverage does not need to be universal for businesses to benefit. Even with partial coverage, PayTo can serve a significant share of customers while other payment methods handle the rest. For a full introduction to the payment method, start with our guide on what PayTo is and how it works.

Customer approval journey

When a business creates a PayTo agreement, the customer receives a notification through their bank. They review the agreement details including the amount, frequency and who is requesting the payment. Once satisfied, they authorise the agreement. The approval is confirmed in real time, allowing the business to begin collecting payments immediately. The experience is designed to be familiar and trustworthy because it happens inside the customer's own banking environment.

Managing agreements in banking apps

Customers can view their active agreements, pause them temporarily, cancel them entirely or approve changes requested by the business. This level of visibility and control is a significant improvement over traditional payment authorities where customers often had limited awareness of active mandates. Empowering customers to manage their own agreements reduces support contacts and builds long term trust.

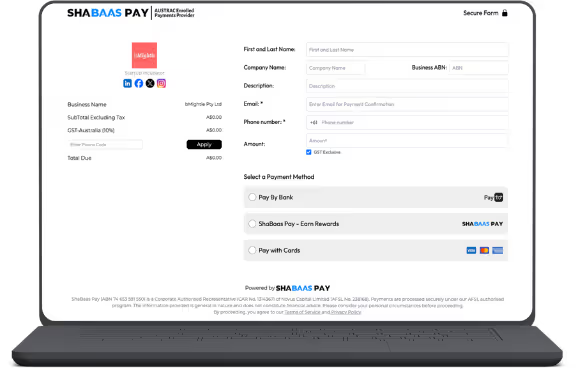

Checkout and invoice messaging

Clear messaging at the point of payment is critical. Businesses should explain what PayTo is in simple terms, confirm that approval happens through the customer's bank and set expectations for what happens next. Avoid technical jargon and focus on trust cues such as bank level security and customer control. For businesses planning their full onboarding flow, the PayTo onboarding checklist covers messaging and UX in detail.

Fallback options

Not every customer will have PayTo available through their bank. Businesses should offer alternatives such as PayID, card payments or invoice links. The key is to present these options clearly without creating confusion. A well designed fallback flow ensures no customer is left without a way to pay and gives the business flexibility as bank coverage expands over time.

.svg)