Key takeaways

- PayTo pricing is typically fixed per transaction rather than percentage based, which benefits higher value payments.

- Total cost of payment acceptance includes fees, failure rates, reconciliation effort and support overhead.

- Card payment costs increase with transaction value while PayTo costs remain predictable.

- Direct debit has lower upfront fees but higher failure and dispute rates that add hidden operational costs.

- Modelling total cost across all payment methods helps businesses choose the right mix.

What drives PayTo pricing

PayTo pricing depends on several factors including provider fees, scheme costs, risk profile and the level of reporting and support included. Unlike card payments where fees are a percentage of the transaction value, PayTo transactions are often priced at a flat rate. This makes costs more predictable and especially attractive for businesses processing higher value transactions. Understanding how PayTo agreements work helps businesses anticipate the volume and frequency of transactions they will process.

Comparing PayTo vs cards

Card payments typically charge a percentage of the transaction value plus a fixed fee per transaction. For a business processing thousands of transactions per month, these percentage fees add up quickly. PayTo offers a different model where costs are usually fixed regardless of transaction size. Settlement is also faster with PayTo, which improves cash flow and reduces the time between service delivery and payment receipt. Reconciliation is simpler with structured references compared to card statement descriptors.

Comparing PayTo vs direct debit

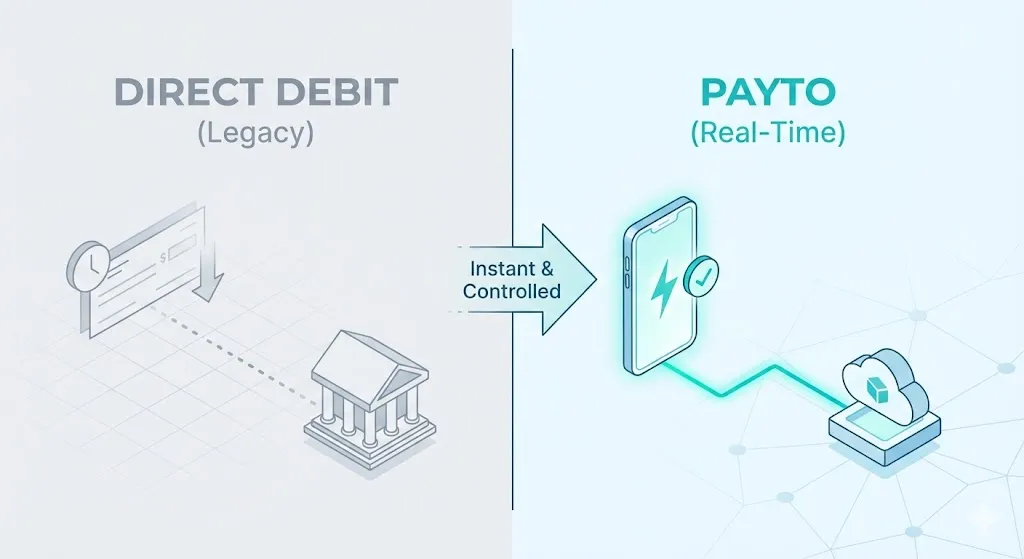

Direct debit has been a standard payment method for recurring billing in Australia. While the per transaction cost is low, businesses often face higher failure rates, slower settlement and limited customer visibility into payment authorisation. PayTo addresses these issues with real time consent, faster settlement and lower dispute rates. For a detailed comparison of how these methods differ in practice, see our guide on PayTo vs direct debit.

How to model total cost

To compare payment methods accurately, businesses should model the total cost using inputs including monthly transaction count, average transaction value, expected failure rate, average support time per failed or disputed transaction and time to cash. A payment method with a slightly higher per transaction fee but significantly lower failure rates and faster settlement can be cheaper overall. Finance teams should revisit this model quarterly as volumes and patterns change.

When PayTo is the best choice

PayTo is particularly well suited for subscription businesses, education providers, professional services firms and B2B invoicing. These businesses benefit from predictable pricing, strong consent visibility and faster access to funds. Businesses already seeing improvements from faster payment settlement will find PayTo a natural extension of their payment strategy. For broader context on how real time payments are shaping the Australian market, explore our overview of real time payments in Australia.

.svg)